Date: June 2026

A £300 order comes in. Before it reaches your account, £7.80 of it is already gone.

On one sale, you’d never notice. But that £7.80 isn’t a flat charge — it’s a percentage, which means it climbs with every order you take and every price you raise. Across thousands of transactions a month, it stops being a fee and becomes something closer to a tax on revenue.

And it’s not one fee.

It’s a chain of them: interchange, scheme fees, processing, acquirer margin, fraud checks, chargeback risk. Each takes its cut quietly, between the sale and the settlement, on every transaction you run.

That is where Pay by Bank starts to matter.

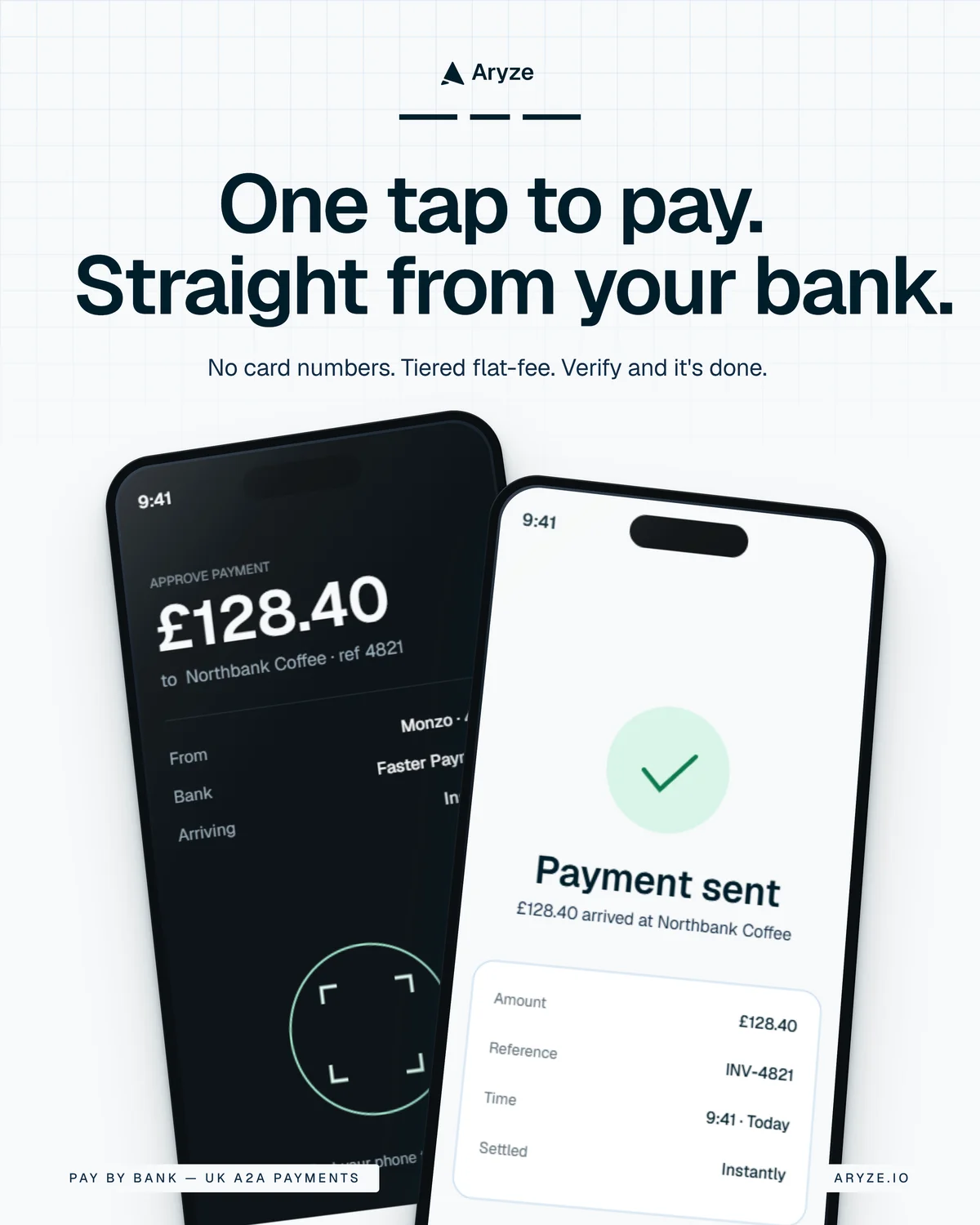

What is Pay by Bank?

Pay by Bank is an account-to-account (A2A) payment method that lets customers pay directly from their bank account.

Instead of entering card details, the customer chooses Pay by Bank at checkout, selects their bank, authenticates through their banking app, and confirms the payment.

For the customer, the experience still feels simple.

For the merchant, the economics can look very different.

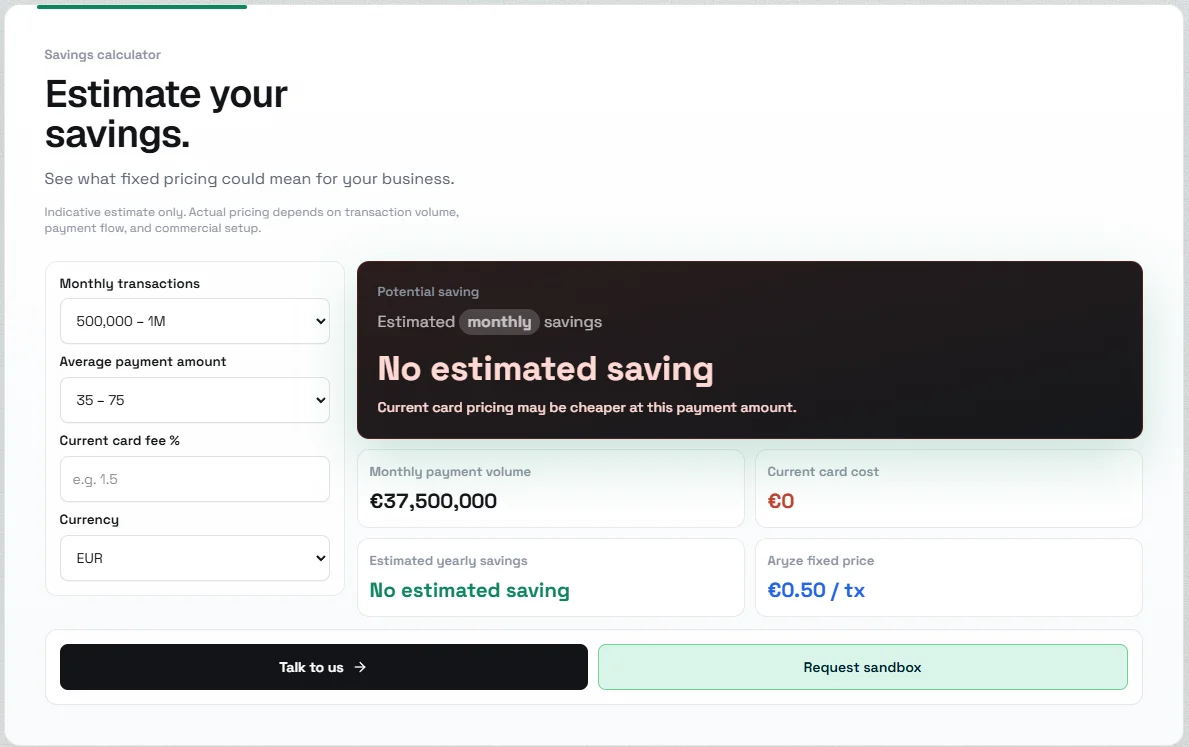

Why the threshold matters

Cards are percentage-based.

That means the cost grows with the value of the payment.

A merchant taking a £20 payment pays a small card fee. The same merchant taking a £200 payment pays roughly ten times more, even though the product, checkout, and operational work are identical.

Pay by Bank works differently.

Instead of charging a percentage of the payment value, the cost is fixed per transaction. A small deposit and a large deposit cost the same to process.

That creates a natural break-even point.

Take a merchant paying a 1.5% blended card rate, with Pay by Bank at £0.50 per transaction. The two costs meet at around £35 — and that threshold shifts with your actual card rate.

Below that ticket size, cards are typically cheaper.

Above it, Pay by Bank pulls ahead and keeps pulling further ahead as ticket size climbs.

What sits above and below the line?

iGaming and betting deposits sit well above the threshold. Trading platform funding events run larger again. For these verticals, the cost gap compounds over annual volume.

Convenience retail, food delivery, and micro-transactions sit below. The card percentage on a small ticket is lower than a fixed A2A fee. No reframing changes that.

Run your own numbers

Enter your monthly transaction count, your average payment amount, and your current blended card rate. The calculator returns indicative monthly and annual savings. Where the math does not land, it tells you so: "current card pricing may be cheaper at this payment amount."

What the math actually tells you

For an operator reviewing payment costs, the conclusion is simple.

If the average ticket sits above the threshold and the blended card rate has climbed over the past few years, Pay by Bank becomes more than another checkout option. It becomes a cost line they can defend at the quarterly review.

If the average ticket sits below the threshold, the answer is different. The rail is not the lever. The conversation moves elsewhere.

Cost is one pressure on a payment stack. Risk is the other — VAMP (Visa Acquirer Monitoring Program) reshaped what that risk looks like in April. The next post is what's showing up six weeks in.

In this series

Aryze · aryze.io · June 2026