Date: April 2026

Margaret is 74.

She is in the process of ordering groceries online when her phone rings.

The caller introduces themselves—polite, professional, and familiar enough to feel believable. They say they're from her bank. There's been suspicious activity on her card. Immediate action is needed.

She hesitates. Then panics.

To “verify her identity,” she reads out her card details.

The caller confirms. The call ends. She feels relieved.

Two minutes later, the groceries are confirmed.

So are three other payments she never made…

This type of fraud is no longer rare. It's a direct consequence of how card payments were designed: sensitive information shared across multiple systems, stored in multiple places, and exposed at multiple points of failure.

Every time a customer enters their card details at checkout, they trust that nothing will go wrong between input and settlement. That trust is increasingly under pressure from rising fraud, growing processing complexity, and systems never built for a fully digital economy.

Pay by Bank is a response to that shift.

What is Pay by Bank?

Pay by Bank is an account-to-account (A2A) payment method that allows consumers to pay directly from their bank account, without a card or digital wallet.

It is powered by open banking technology, which uses secure APIs facilitated by regulated Payment Initiation Service Providers (PISPs) to connect a merchant's payment system to a customer's bank.

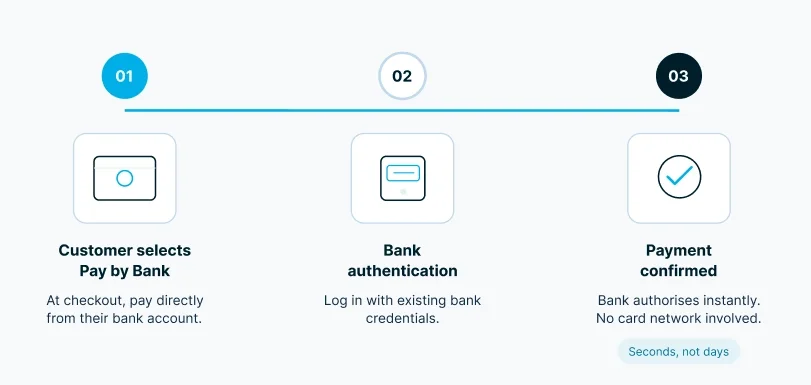

The customer experience is straightforward:

No card number is entered. No sensitive data is shared with the merchant.

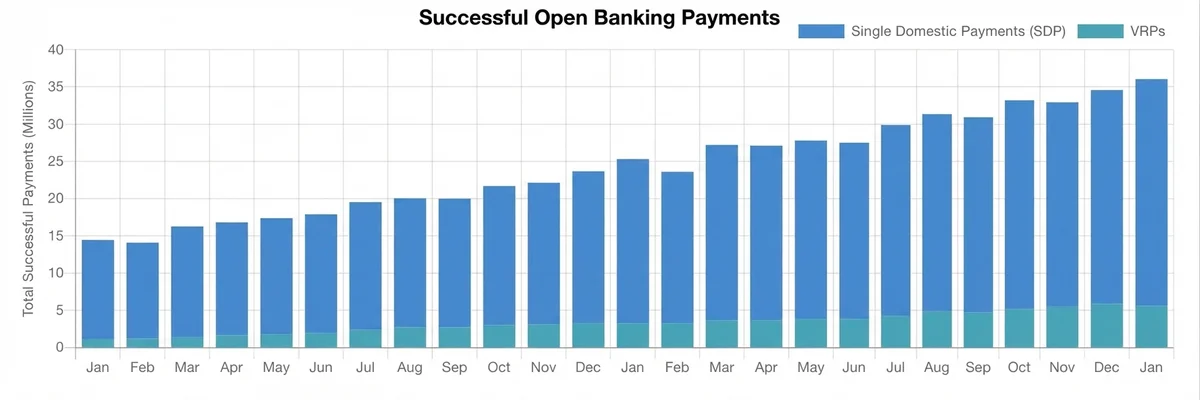

This is not a workaround or a niche solution. It is a regulated, infrastructure-backed payment method that is growing rapidly across Europe and beyond, supported by frameworks like PSD2 in Europe and open banking mandates in the UK.

Why It Matters for Merchants

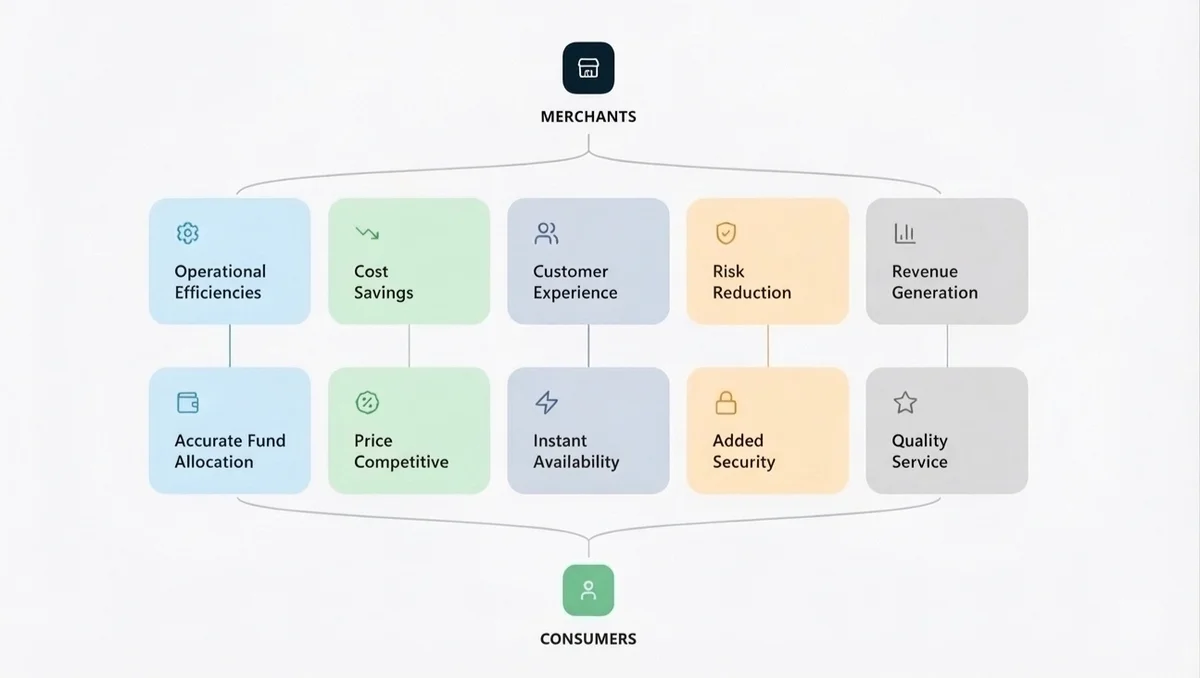

Pay by Bank from a merchant perspective comes down to three things:

Card payments carry interchange fees, scheme fees, and acquirer margins that add up quickly, particularly for high-volume or high-value transactions.

Pay by Bank removes the card networks from the equation entirely. Payments move directly between bank accounts, which means significantly lower transaction costs.

Because your customer authenticates the payment directly with their bank using strong customer authentication, the risk of fraud is substantially reduced.

Funds move in real time or near real time, depending on the payment rail — improving cash flow without relying on card network settlement cycles.

Why It Matters for Consumers

For consumers, Pay by Bank removes the need to share card details with merchants they may not fully trust. Authentication happens inside their own banking app, an environment they already use daily. Nothing new to download. No account to create. No card details to remember (or update when a card expires).

It also gives consumers a clearer view of their spending. Because payments come directly from their bank account, the transaction appears immediately in their banking app, making budgeting and reconciliation more transparent.

How Aryze Helps

At Aryze, we have built Pay by Bank into a clean, reliable payment flow that works for merchants across industries, including those that traditional card processors have historically underserved.

Our solution connects directly to customers' banks using open banking infrastructure, delivering:

Whether you are a high-volume e-commerce business looking to reduce processing costs or a high-risk merchant seeking a stable, compliant payment alternative, Pay by Bank through Aryze is built to meet your needs.

The infrastructure is in place. The regulation supports it, and customer behaviour is shifting. The question is not whether Pay by Bank will become a mainstream payment method — it is whether your business is ready for it.

Aryze · aryze.io · April 2026